A traditional bonus is heavily taxed and subject to very high social security contributions (NSSO).

By converting the bonus into warrants, the employee and employer are exempt from social security contributions, and the employee's net can be increased by up to 45% (warrants) or up to 90% (long-term options) via a partial or total retrocession of the employer's social security contributions to the employee.

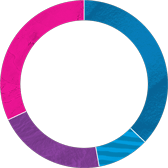

Cash bonus

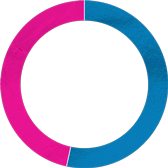

Short term warrants

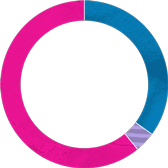

Long-term options

net

Taxes

NSSO Employee

NSSO Employer

Loss of time value

Warrants plan (short term)

NO employer/employee social security contributions

Blocking period: 8 hours

Increase in net remuneration of around 45% compared with the classic cash bonus

Long-term options plan

NO employer/employee social security contributions

Advantageous flat-rate tax

Blocking period: 12 months

Increase in net remuneration of around 90% compared with the classic cash bonus